The numbers are in and it’s not pretty…

Comercam released its annual Informe and if you have been reading our newsletter you already knew production numbers were going to be down. What is surprising is by just how much.

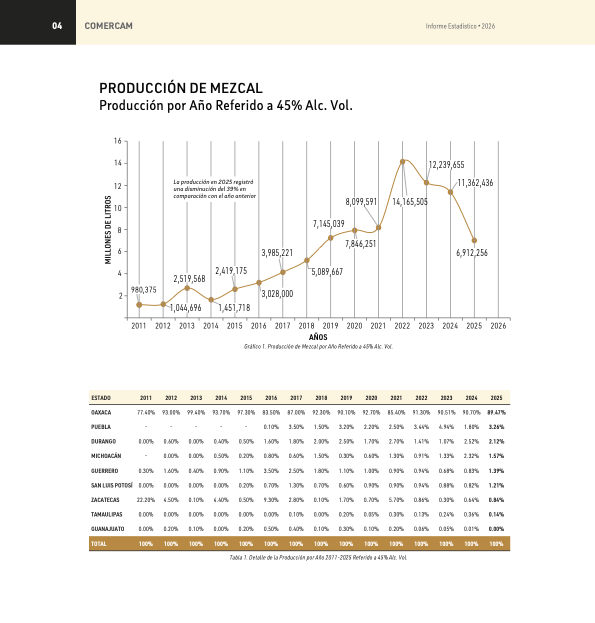

From conversations with mezcal producers we knew that there was a slowdown in production because orders had slowed in 2025 and there was already a lot of mezcal sitting on the ground. But that steep decline of almost 40% was a bit of a shock, even when comparing to 2019 (a decline of 2.8%), what we refer to as the last “normal” year. This is not a sky is falling comment, but it does speak to just how much of an impact general economics, decline in alcohol consumption, and the overall market dynamics (distribution issues, challenged on-premise market, etc) are having on mezcal sales. And while it might not seem like much, it’s interesting to note the near 100% growth in production in Puebla, San Luis Potosi, and Guerrero.

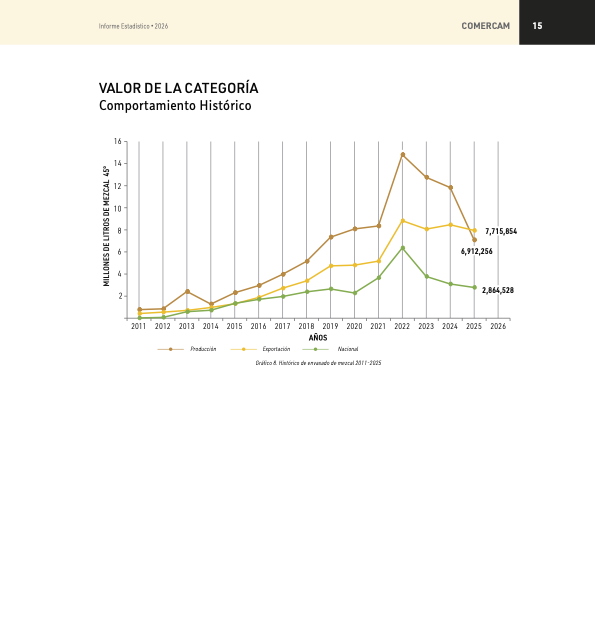

It’s also interesting to look at the numbers for both the national and international markets as compared to the overall production numbers. These numbers show what has been bottled and sold into those markets. They are greater than what was produced overall in 2025, 10.6 million liters vs 6.9 million liters produced, a difference of 3.7 million liters-which speaks to the overall inventory of mezcal on the ground in Mexico. These numbers also continue to track above the 2019 numbers. It is yet another indicator of just how distorted production was during the pandemic and how long it is taking to move into “normal.”

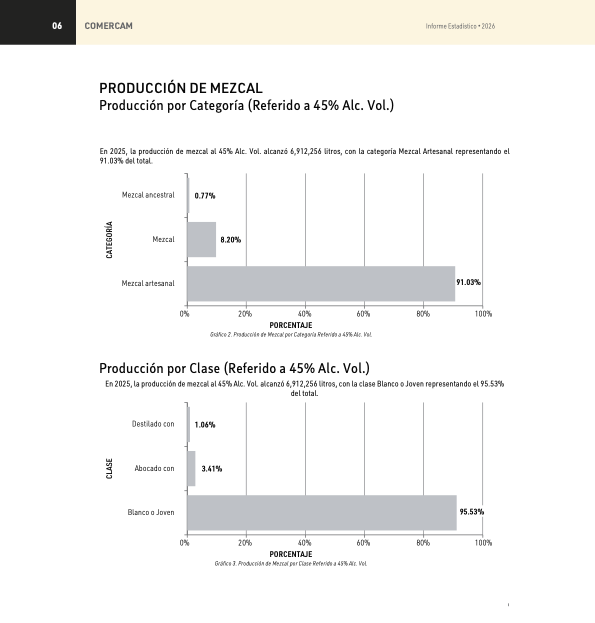

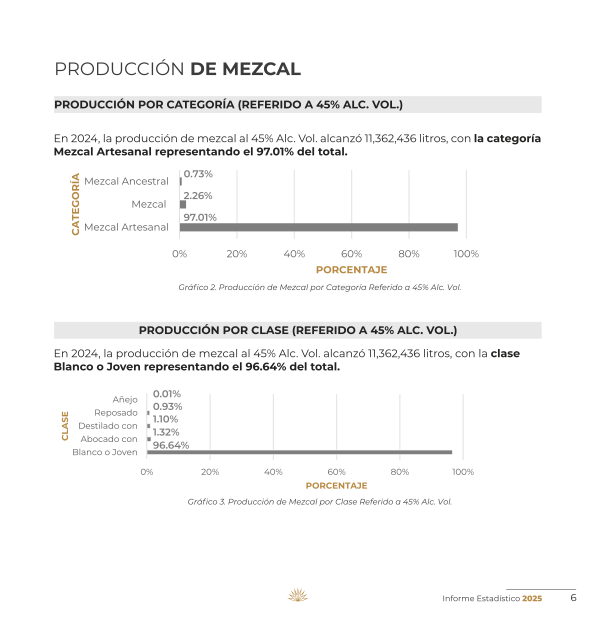

In looking at numbers across category and class, 2025 saw a near fourfold increase of production in the Mezcal category from 2024, which is the category that allows for more industrial practices. Also of note, a near threefold increase in the Abocado con (infused with) class in 2025, though it is possible that class now includes añejo and reposado classes which were not broken out in the 2025 numbers.

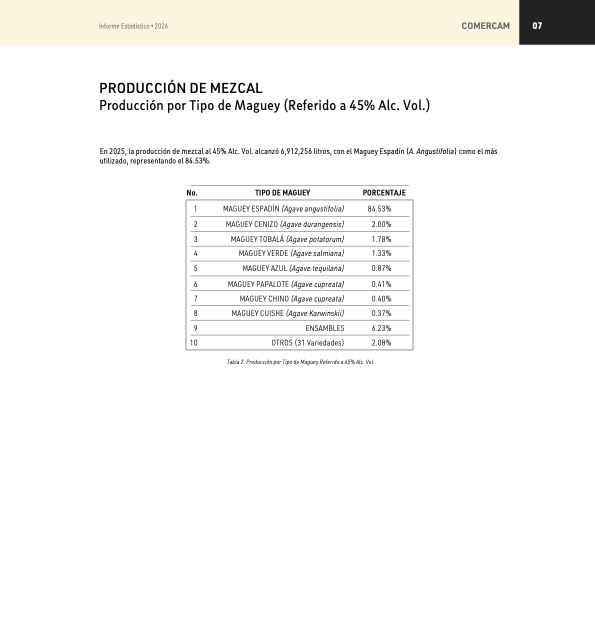

In terms of agave, Espadín remains queen–consisting of 84.5% of mezcal production.

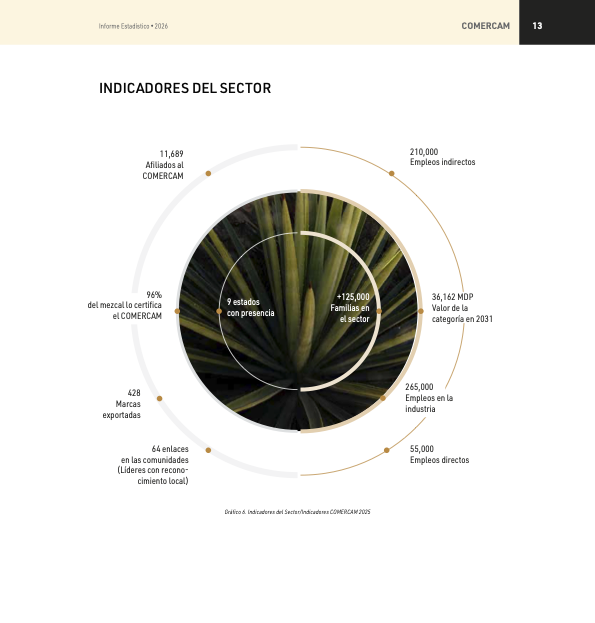

Finally a few other indicators Comercam tracks that include total direct and indirect employment in the sector (55,000 and 210,000 respectively), brands exported (428) and the number of families (125,000) involved in the making of mezcal. These numbers remain relatively unchanged from 2024.

There is no doubt 2025, and so far 2026, remain challenging. This is a market currently driven by price, with mezcals priced below $50 (retail) dominating sales. Since those are mezcals concentrated among 5-8 brands, think of a market that is increasingly dominated by cocktails and brands that have national distribution. It is therefore incumbent upon consumers to determine the diversity of the market. In other words, maybe focus on drinking quality, even if it costs a little bit more.

Or as Comercam concludes:

“The year 2025 offered a clear lesson for the mezcal industry: growth is not linear, yet the sector’s strength can be sustained through consistency and clear direction.

In an international environment marked by contraction, the figures reflect an adjustment in market dynamics. However, beyond the results, this period tested the production chain’s

adaptability and the resilience of the institutions supporting it.

Against this backdrop, the strategy went beyond merely maintaining operations; it focused on creating conditions that allowed the sector to remain active, visible, and competitive.

Mezcal’s presence was strengthened in both domestic and international arenas, bolstering its positioning as an iconic Mexican spirit—one deeply rooted in its communities and an

enduring legacy.”

Leave a Comment